Section

Navigation

Section

Navigation

9. Learning from Others

9.1 Introduction: Grouping by Business Models

:Cautionary Tales

9.2 A Start

9.3 Coins International

9.4 Fine Art Ceramics

9.5 Halberd Engineering

9.6 Ipswich Seeds

9.7 Seascape e-Art

9.8 Whisky Galore

:Case Studies

9.9 Amazon

9.10 Andhra Pradesh

9.11 Apple iPod

9.12 Aurora Health Care

9.13 Cisco

9.14 Commerce Bancorp

9.15 Craigslist

9.16 Dell

9.17 Early Dotcom Failures

9.18 Easy Diagnosis

9.19 eBay

9.20 Eneco

9.21 Fiat

9.22 GlaxoSmithKline

9.23 Google ads

9.24 Google services

9.25 Intel

9.26 Liquidation

9.27 Lotus

9.28 Lulu

9.29 Netflix

9.30 Nespresso

9.31 Netscape

9.32 Nitendo wii

9.33 Open Table

9.34 PayPal

9.35 Procter & Gamble

9.36 SIS Datenverarbeitung

9.37 Skype

9.38 Tesco

9.39 Twitter

9.40 Wal-mart

9.41 Zappos

9.42 Zipcar

9.14

Commerce Bancorp, Inc.

9.14

Commerce Bancorp, Inc.

Commerce Bank, also known as Commerce Bancorp, and more familiarly as

'America's Most Convenient Bank', was a leading retailer of financial

services with over 450 convenient stores in New Jersey, New York, Connecticut,

Pennsylvania, Delaware, Washington DC, Virginia, Maryland and Florida.

Headquartered in Cherry Hill, NJ, Commerce Bancorp (NYSE: CBH) had $50

billion in assets.

In October 2007, the TD Bank Financial Group acquired Commerce Bank in a 75% stock and 25% cash transaction valued at US$8.5 billion. Under the agreement, Commerce shareholders received 0.4142 shares of a TD common share and US$10.50 in cash in exchange for each common share of Commerce Bancorp Inc. The consideration was negotiated on the basis of US$42.00 per share value for Commerce Bank. {1}

Background

US retail banking is a mature and highly competitive business where improvements in rate differentials or services are quickly matched. Many mid-tier banks were acquired or squeezed out in the 1980s and 1990s, leaving local communities with a restricted choice. To meet acquisition costs, the larger banks have generally displeased their retail customers by:

1. Targeting richer customers with bundled investment offerings.

2. Offering more basic and standardized service to other customers.

2. Replaced personal services by cheaper ATM and Internet services.

By 2001, surveys indicated that only 53% of retail customers were satisfied with their bank. Disaffected customers shopped around, and the larger banks lost a third of customers each year.

America's Convenience Bank

Commerce Bancorp set out to counter this tendency by focusing on the customer. The bank: {1}

1. Thought like a retailer and designed banks with roaming tellers

and children's play areas.

2. Built a 'customer first' approach into everything, from selection

of front-line employees to staff training.

4. Opened at hours convenient to customers: weekends and evenings.

5. Offered the usual services but made them responsive: fees were reimbursed

for out of network ATMs, for example.

6. Stayed close to parity on the price value vector (see below) but

didn't attempt to match their lowest-priced rivals.

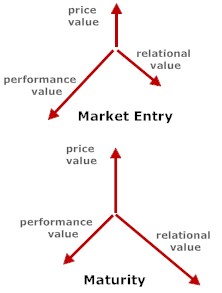

Value Vectors

When able to do so, customers opt for better value, but that better value can be price, performance, or relational value. {1}

Price value covers:

1. Best price for a standard product.

2. Acceptable quality.

Performance value covers:

1. Better functionality.

2. Innovative features.

3. Improved quality.

4. Superior design.

Relational value covers:

1. Personalized treatment.

2. Products tailored to the customer's needs.

3. Integrated solutions.

4. All-round service excellence.

Typically, as a product or service matures, its value vectors change in their importance.

Outcomes

Until taken over by the TD Financial Group, Commerce Bancorp:

1. Expanded rapidly, from 150 branches to 450 over the 1999-2008 period.

2. Achieved an average annual revenue growth of 28% and annual asset

growth of 36% over the 1999-2008 period.

3. Grew deposits from $5.6 billion to $27.7 billion over the 1999-2004

period.

4. Increased loans from $3 billion to $9.4 billion over the 1999-2004

period.

5. Grew deposits by nearly 40% in 2001, against a nationwide average

of 5%.

6. Cut its customer defection rate to half that of its larger rivals.

Questions

Questions

1. What has the banking sector generally done to cover acquisition

costs? How was Commerce Bancorp different?

2. What are value vectors, and how do they generally evolve with market

sector maturity?

3. Given that Commerce Bancorp was eventually taken over by another

bank, in what sense was its business strategy successful?

4. What elements of Osterwalder and Pigneur's business model throw light

on Commerce Bancorp's strategies?

Sources

and Further Reading

Sources

and Further Reading

1. Strategy from the Outside In by George S.

Day and Christine Moorman. McGraw Hill. 2010. 56-61.

2. Company History. TD

Bank. Brief history of Commerce Bancorp acquisition in 2008.

3. TD mascot sporty, fun and 'strains intellectual scrutiny'

by Jeff Blumenthal. Philadelphia

Business Journal. October 2010.

4. Commerce Bank. Federal

Reserve Financial Services. January 2007.

5. Commerce Bank New Jersey. Lycos

Retriever. Helpful archive of articles but repetitive.

6. TD Bank in US push with $8.5bn deal by Ben White. FT.

October 2007. Reasons behind acquisition by Toronto Dominion Bank.