Section

Navigation

Section

Navigation

3. eBusiness Prospects3.1 B2C: North America

3.2 B2C: South America

3.3 B2C: Europe

3.4 B2C: Middle East & Africa

3.5 B2C: Asia

3.6 B2B

3.7 m-Commerce

3.8 Modeling Trends

3.9 USA forecasts

3.10 China forecasts

3.11 EEC forecasts

3.12 India forecasts

3.13 Japan forecasts

3.14 UK forecasts

3.15 Russia forecasts

3.16 Brazil forecasts

3.17 World forecasts

Sources

Sources 3.14

United Kingdom

3.14

United Kingdom

Britain began the industrial revolution, and dominated the world economy during most of the 19th century. The country was a major innovator in machinery, railways, steamships, textile equipment, and tool-making equipment, inventing the railway system and producing much of the equipment used by other countries. It also led in international and domestic banking, entrepreneurship, and trade, accumulating a world empire in the course of its century-long rivalry with France. Originally protectionist, Britain practiced 'free trade', with no tariffs or quotas or restrictions after 1840. Between 1870 and 1900, the GDP per capita rose 500 per cent, generating a significant rise in living standards. Thereafter the country was gradually overtaken by the USA and Germany. GDP per capita in 1870 was the second highest in the world (after Australia). By 1914, it was fourth highest. {1-7} In 1950, British output per head was still 30% ahead of the six founder members of the EEC, but by 2000 it had fallen behind the USA, many European countries and several in Asia. {7} The twentieth-century economic history of Britain is commonly divided into: {6}

1920s: war debt, deflation

and life under the gold standard.

1930s: mass unemployment.

1940-50s: austerity,

rationing, war debt, but full employment, new welfare state and rising living standards.

1960s: confidence, prosperity and alternative cultures.

1970s: era of discontent:

strikes, 3 day weeks, inflation, boom and bust.

1980s: Thatcher years of monetarism

and financial deregulation, two deep recessions, mass unemployment, and then boom.

1990s: recession and then the great stability.

2000s: financial innovation and

deregulation, housing boom — leading to bank/building society collapses and government

bailouts.

2010s: austerity and recession.

SWOT Analysis

Strengths {8}

Leading trading nation

Highly efficient

agricultural sector

Recognized strengths in banking, insurance, and business services

(comprising 75% of GDP)

Generally good industrial relations

Strong IT industry

Politically stable

Good educational standards

Vibrant culture

Speaks

the world language of business

Stable and growing economy

Still one of the

largest recipients of foreign direct investment

Weaknesses

Transport

system antiquated and expensive

Shortage of skills

Reputation for innovation

but generally insufficient R & D

High levels of government and personal debt

Opportunities

Entry

point for US investments into Europe

Banking reform

Internal Threats

High

debt levels

Financial crisis

Strengths: Financial Services

Gold Standard

Though often relegated to a footnote in economic histories, possibly unwisely, {9} the gold standard was the world's first attempt at a universal currency, establishing the city of London as a center of financial services, a reputation it still enjoys today. The 1870-1914 period of the gold standard brought unparalleled wealth and stability for members of the club, in which there were few examples of currency manipulation, inflation or balance of payment problems. {11} No central or world bank was needed. Simple telephone calls enabled financial centers in Paris, New York and Buenos Aries to conduct business with a reasonable amount of trust. All currency was underwritten by gold reserves, and any profligacy corrected by gold flows. Several nations, including England and the Netherlands, had used a gold standard previously, but the club was joined by Germany and Japan in 1871, France and Spain in 1876, Argentina in 1881, Russia in 1893 and India in 1898. The US, though minting gold coins since 1832, did not formally join until the Gold Standard Act of 1900.

Most countries had come off the gold standard during W.W.I when they needed to print large amounts of money to pay for troops and armaments. The new gold standard agreed by participating countries at the Genoa Conference of 1922 was a nominal one, which simply accepted that foreign exchange balances would be treated as gold for reserve purposes. Gold only nominally backed American currency, for example, and money supply was in the hands of the Federal Reserve System, created in 1913 to bail out defaulting banks. The yellow metal was then valued at US$20.67/ounce, but gold coins and bullion no longer circulated, and any exchange of gold for paper currency was in minimum quantities, typically 400 ounce bars, which largely restricted use to interbank dealings. International dealings became unstable under this 'gold exchange standard', as regulation was dependent on countries playing by certain rules. Not all could afford to. The French franc crashed in 1923. Britain returned to the prewar gold parity, a massively deflationary measure that created widespread business failures and added millions to the unemployed. In time, of course, accumulating trade surpluses by the more successful countries led to demands to 'see the money', i.e. hand over the gold. Both America and Britain found their gold reserves being rapidly depleted, and it was to sever this difficult relationship that Roosevelt in 1933 took gold out of contention. Gold was forcibly purchased from US citizens at its existing price, and its ownership (beyond a few trifling exceptions) made illegal. Banks were closed and confidence restored by having their accounts audited. When the gold price was finally set at $35/ounce, the dollar had been drastically devalued, and American exports made more competitive. Yet, for all so controversial a measure, the effect was short-lived, and US full unemployment had to wait to W.W.II. {11}

The Bretton Woods accord of 1944-5 fixed exchange rates and achieved some price stability for twenty years. But then came the UK sterling crisis of 1967, when many factors (rising unemployment, balance of payment problems, currency adjustment to possibly join the EEC, and more - see below) caused the British Government to devalue the pound sterling from $2.80 to $2.40 to the dollar. Bretton Woods no longer seemed so secure, and there was a rush to buy gold, particularly from the London Gold Pool, which saw large outflows. By March 1968, sales of gold were running at thirty metric tons an hour, and the Pool shortly afterwards collapsed. A new international reserve asset was conjured up by the IMF a year later: special drawing rights (SDR: essentially a paper exercise that shared responsibilities among IMF members according to their assets) but the period to 1971 was one of great uncertainty. President Nixon's announcement on August 15, 1971 was part of a New Economic Policy of immediate wage and price controls, a 10% surtax on imports and the closing of the gold window (the mechanism whereby the dollar was converted into gold by foreign central banks).

It was none too soon. Trade deficit with Japan and Europe had reduced US gold reserves to 9,000 metric tons by 1971 (and those in the UK were only 609 metric tons). Nixon's intention was to make American exports more competitive by lowering the value of the dollar, and the surtax was to be removed once that had been achieved. The Japanese allowed the yen to float, when it rose 7% against the dollar. With the 10% surtax, the American dollar had been devalued by 17% against the yen, so helping to reverse the trade deficit. Canada and the European countries particularly disliked the surtax, however, which they saw as creating severe unemployment in their respective countries, and, after much haggling, the G10 meeting agreed a 9% devaluation of the dollar against gold, a revaluation of European currencies against the dollar of 3 to 8%, and a removal of the surtax if countries kept exchange rates within a 4.5% trading band. Again, though popular at the time, the Nixon plan did not bring lasting success. Other countries made their own adjustments and within two years the USA found itself mired in recession. {11}

The gold standard prior to 1971 did not, of course, allow someone to purchase an ounce of gold by handing over $35 at their local bank. That $35 had anyway been devised by Roosevelt to devalue the dollar and make it more competitive. The price was nominal, and another change in price could have 'backed' the dollar without increasing the supply of gold. Set the price at $350, and ten times the previous amount of money is 'covered'. James Rickard {11} indeed has argued for a return to the gold standard, though with gold more highly valued, and heavy taxes to offset windfall gains. Few economists are today interested in the gold standard, however, and such a large price increase would greatly increase gold supplies from currently uneconomic deposits, a development that would again need unusually wide taxation consensus.

Though nearly half the foreign exchange markets prior to 1913 involved pound sterling, the leading exchange markets (forexes) were not located in London but Paris, New York and Berlin. {27-9} When the Breton Woods Accord ended in 1973, and currencies were allowed to float, the balance shifted to the UK (with the USA in second place), a shift facilitated by financial deregulation (the 'Big Bang') and the introduction of Reuters computer monitors, which replaced the previously used telephones and telexes. Turnover of exchange-traded foreign exchange futures and options have grown rapidly in recent years, reaching $166 bn in April 2010 (double that of April 2007). London remains the world's greatest foreign exchange market, much of the activity being located in the City of London. The average daily turnover in April 2011 was US$2,042 bn, some 37% of the world total. The breakdown was as follows: $1.490 trillion in spot transactions, $475 billion in outright forwards, $1.765 trillion in foreign exchange swaps, $43 billion currency swaps, and $207 billion in options and other products. {29}

What conclusions can be drawn from this digression into the history of the gold standard?

1. Today's financial world is necessarily 'dog eat dog'. Banking may verge on sharp practice, but, as presently constituted, allows no alternative: 'when the music starts everyone has to get up and dance'.

2. Large sums are traded, and the increasing instability is such that major errors may quickly wipe out banks and businesses.

3. Money is closely tied to politics. De Gaulle, for example, had accused policymakers of exporting US inflation to France. America had printed dollars to cover Vietnam War expenditures, but not devalued its currency, requiring France to accept the weakened dollar at face value. To force the issue, France passed legislation in 1967 that re-established a franc backed by 80% of gold reserves, at the same time withholding its own gold from sale through the usual London gold pool. So arose the 'sterling crisis'. Speculators immediately sold sterling and bought gold wherever available, causing a run on the British currency. When other countries and the IMF would not support the pound further, Britain was obliged to devalue by 14%, fixing the pound at 2.40 to the dollar, and bringing pressure to bear on the overvalued dollar. US banks in turn engineered a run on French banks, replacing franc holdings by German marks, got the government to restrict French imports, and ensured the media gave full coverage the 1968 Paris uprising. De Gaulle's standing was badly damaged, and he resigned in April 1969. {30}

Business, in short, may be better approached through underlying political realities than by 'business news' and market studies, important though these are.

Outlook: Mainstream Views

Britain has only slowly adjusted to its loss of empire. {22-26} Services took precedent over manufacturing, and financial services currently employ over a million people, accounting for 9% of UK GDP and 12% of UK tax receipts. Their contribution to GDP (8.8%) is higher than that of other advanced nations (USA 8.4%, Japan 5.8%, Germany 8.3% and France 5.1%). UK fund managers hold £3.2 tn in financial assets. Foreign companies invested £33 bn in the UK financial services sector between 2008 and 2010, more FDI than in any other sector of the economy. Of the 953 foreign companies authorized by the FSA in 2010, 420 were US-owned. {12}

Online transactions more than doubled to nearly 6 billion between 2005 and 2010, {12} but London's GVA (gross value added) in financial & insurance activities fell by 2.2% in 2010, growing by 1.5% in 2011 but expected to grow by only 0.1% in 2012. {13} Though not part of the eurozone, London's performance is much influenced by the global economy, and financial & insurance activities are indeed forecast to slow to a halt as the eurozone crisis damages investor confidence. The higher liquidity and capital requirements in Basel III, the required separation of retail and investment banking, and the general restructuring of bank operations are further threats. {27-29}

Outlook: Models

Under its unpopular coalition government, the UK has adopted both the EEC austerity approach and the US preferential treatment of banks.

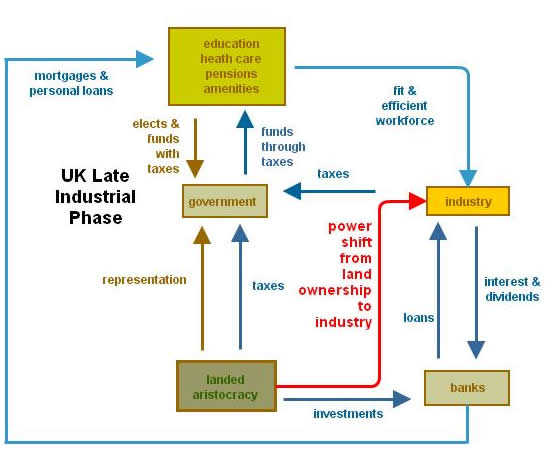

Michael Hudson's analysis of the US

scene {31} therefore applies to the UK, and recognizes a two-century- long industrial

phase where governments have taxed the 'unearned' income from land rent and natural

resources to provide a higher standard of living to the workforce employed in mines,

farms, businesses and industries.

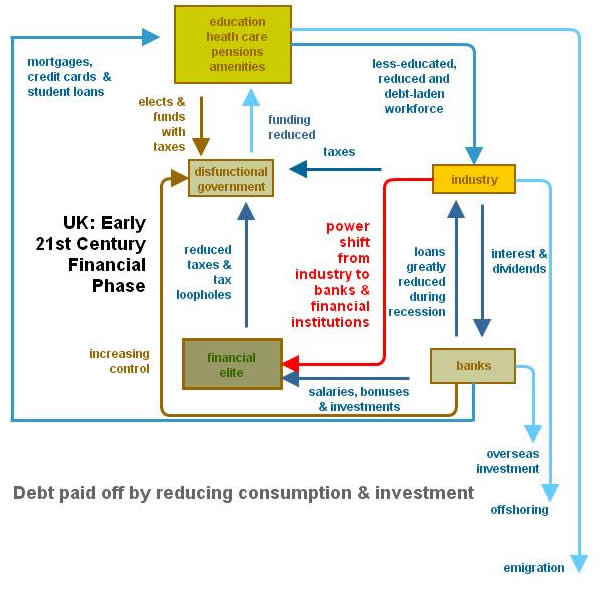

Starting with the Thatcher years, however, the model has been reversed, with the banks and financial institutions gaining the power formerly enjoyed by the landed aristocracy. Failing banks have been bailed out with taxpayers' money (with the government obtaining a voice in their management, however). Public services have been privatized and/or cut back. Debt has been increased by the Bank of England's quantitative easing /printing money, and the orthodox economics appearing in university courses and business magazines has become an instrument of power, making no distinction between productive (investment in industry, innovation and training) and nonproductive (capital gains in land prices, stocks and bonds). UK economic performance has been unexciting, {34} and the country currently faces a triple-dip recession. {35}

Hudson's remedies are simple, but unlikely to prevail against established interests.

1. Redeem

debt that can't be repaid sooner than later. Some banks will doubtless fail, but are

not socially productive.

2. Educate the voting public (and economics students)

in the current dynamics.

3. Remove favorable tax rates on capital gains.

4.

Reverse privatization and sell-off of public services.

The forecast is for increased inflation as the financial elite bid up land prices and stocks — coupled with deflation as interest payments reduce expenditure on goods and services. Something similar to Japan's 'lost decade' is possible, and it's worth noting the widespread riots of 2011, {32} and that ten percent of British nationals now live abroad. {33}

eBusiness Implications

Internet banking in the UK is on the rise: 55% of all adults use the facility, rising to 72% in the 24-35 age bracket. Banks are improving security (virus protection, strong encryption and/or portable card reader or a secure code generator device) but fraud losses were reported at £16.9 million in the first half of 2011, admittedly down 32% from the previous year. The UK does not have the highest Internet access in Europe, however, nor the highest use by business. {14} UK online banking also suffered well-publicized failures in 2012, suggesting limits to staff reduction and outsourcing. {15}

Trading IT revenues at the largest exchange operators are estimated to grow from US$1.8 bn in 2011 to US$3.8 bn in 2015. {28} Indeed the London Stock Exchange had to change its in-house core trading platform in late 2009, from one developed in .Net ( Tradelect) when this Microsoft platform could no longer cope with the increasing number of investment banks using algorithmic trading software, nor the increased competition from traditional exchanges. Tradelect had gone live in June 2007, on time and within budget, for £40 million outlay. The replacement was the Sri Lanka Millennium IT system running on Linux, where the Exchange bought not just the software but the whole company (for £18 million). During the 15 month migration from Tradelect, the Exchange also took control of a competitor, Turquoise, so acquiring the technology for multilateral trading facilities (MTFs) that sprang up after the introduction of the FSA's Markets in Financial Instruments Directive (Mifid). Turquoise allowed traders to trade off-the-exchange, where their activity cannot be seen by other traders, in a trading environment known as a 'dark pool'. {20-21}

MillenniumIT enabled the adoption of a software development process called 'BID' (business innovation-dynamically), which splits the development into three parts: 1. the hardware and operating systems, 2. the application layer (trading platforms, ERP and clearing systems) and 3. the business controls on top. The system is faster, easier to write programs for, and costs less — all important when stock exchanges regularly have to tweak systems to meet regulatory and business changes. {20-21}

Competition drives not only the companies listed, but the exchanges themselves, and the new technology is claimed to have saved the London Stock Exchange from hostile takeover. The Exchange is in merger talks with the Toronto Exchange to create an exchange worth £3.7 tn, while Deutsche Borse and NYSE are also talking about coming together. {17} Critics have naturally questioned the City's continuing involvement in risky derivatives,{18} arguing it spells only trouble ahead, but the industry has lobbied successfully {19} for UK financial services not to be regulated in the manner increasingly adopted by the eurozone countries. {22}

Why the intense competition? Consider the Porter's five forces model. The entry barriers are weak, the others strong, making great rivalry to be expected:

Supplier power: large: expertise: most banks have or can acquire the know-how.

Entry barriers: low: most financial centers have access to this level of capital.

Substitution threat: large: new types of derivatives are being devised all the time.

Buyer power: large: capital is globally fluid.

Points

to Note

Points

to Note

1. First mover advantage, and the social costs of the industrial revolution.

2. Growth under a protectionist economy, 'free trade' being adopted later, from a

commanding advantage.

3. Technological enablement: London is the leading forex.

4. Relentless competition in financial services: stay ahead or be taken over.

Sources

and Further Reading

Sources

and Further Reading

1. The British Industrial Revolution

in Global Perspective by Robert C. Allen. C.U.P. 2009.

2. The Origins of

the Modern World: A Global and Ecological Narrative from the Fifteenth to Twenty-first

Century by Robert B. Marks. Rowman and Littlefield, 2007.

3. The Human

Web: A Bird's-Eye View of World History by J.R. McNeill and William H. McNeil.

Norton 2003. Chapter 7.

4. The Origins of the Industrial Revolution in England

by Steven Kreis. History

Guide. 2001.

5. Causes of the Industrial Revolution by Eric Bond,

Sheena Gingerich, Oliver Archer-Antonsen, Liam Purcell, and Elizabeth Macklem. Industrial

Revolution. February 2003.

6. UK Economic History by Tejvan Pettinger.

EconomicsHelp.

March 2010.

7. Economic history of the United Kingdom. Wikipedia.

September 2012.

8. Swot Analysis of the UK. Oppapers.

Accessed October 2012.

9. Aware of Price Manipulation, China Fighting Dollar

With Gold by Alex Newman. New

American. September 2011.

10. The Ascent of Money by Niall Ferguson.

Penguin, 2008.

11. Currency Wars: The Making of the Next Global Crisis

by James Rickards. Penguin, 2011. Chapter 3.

12. Economic Contribution of UK

Financial Services 2010. TheCityUK.

April 2012. Lobby group, but with good statistics.

13. The Economic Outlook

for London. CityofLondon.

April 2012.

14. Information society statistics. EC

Eurostat. September 2011.

15. RBS-NatWest bank meltdown rolls on: Chaos

to hit millions all weekend, customers still can't get wages - and it may last until

next week by Ed Monk and Andrew Oxlade ThisIsMoney.

June 2012.

16. How Online Trading Works by Tracy

V. Wilson How

Stuff Works.

17. Raging Bulls: How Wall Street Got Addicted to Light-Speed

Trading by Jerry Adler. Wired. August 2012.

18. Britain's financial industry:

Death by a thousand cuts. Economist.

January 2012.

19. London's financial lobby machine sways UK policies: report.

Reuters.

Juky 2012.

20. London Stock Exchange completes 15-month system replacement.

Computer

Weekly. March 2011.

21. Millennium SQR.

Millennium. 2010. Brief white paper.

22. David Cameron under pressure

to veto EU power grab. Daily

Telegraph. June 2012.

23. Britain's decline; its causes and consequences

by David Owen. March 1979. Economist.

June 1979.

24. The 'managed decline' of Britain by David Jamieson. Counterfire.

January 2012.

25. Empire: The Rise and Demise of the British World Order and

the Lessons for Global Power by Niall Ferguson. Basic Books 2004.

26. The

Blunt Axe by Peter Allen.

Lombard Street Research. September 2012.

27. Foreign exchange market.

Wikipedia.

August 2012.

28. Exchanges 2.0: The Evolution of Exchange

Technology in Cash Markets. Celent.

August 2011.

29. A review of the work of the London Foreign Exchange Joint

Standing Committee in 2011. Bank

of England. Q2 2012.

30. Gods of Money: Wall Street and the Death of the

American Century by F. William Engdahl. EditionEngdahl 2010. Chapter 13.

31.

The Bubble and Beyond: Fictitious Capital, Debt Deflation and Global Crisis

by Michael Hudson. Islet. 2012.

32. UK riots and social media by Jim Killock.

Open

Rights Group. June 2012.

33. It's young workers, not retirees, looking

to move abroad. Daily

Telegraph. December 2012.

34. UK economy: Stuck in low gear by Chris

Giles. F.T.

October 2012.

35. UK drives triple dip recession fears. Financial

Express. January 2013.