Section

Navigation

Section

Navigation

8. Models and Strategy

8.1

eBusiness in Context: US Scene

8.2 Strategic

Management

8.3 Grouping by Strategy

8.4 Business Models

8.5

Customer Segments

8.6 Customer Channels

8.7 Customer Relationships

8.8 Key Resources

8.9

Key Partnerships

8.10 Key Activities

8.11 Value Propositions

8.12

Cost Structure

8.13 Revenue Streams

8.14 Internet Revenue Models

8.15

Strategy

8.16 Company Valuation

8.17

Measures & Ratios

8.18 Fundamental

Analysis

8.19 Efficient Markets

8.20

Neoclassical Economics

8.20

Neoclassical Economics

8.20

Neoclassical Economics

Once the center of economic thought, and sure of a place in every business studies textbook, neoclassical economics now finds itself under attack from many quarters.

Hence this introduction to alternative views, a suggestion that readers use some critical judgement in reading the standard business studies textbooks and mainstream news outlets like Businessweek, the Financial Times, Wall Street Journal and the Economist. {1-4}

Introduction

Economics is a science: the study of the allocation of scarce resources. It is unlike other sciences in deducing effects from models, rather than inducing laws from observation. Neoclassicism sees itself as objective, however, allowing practitioners with the same procedures to draw the same conclusions from evidence agreed to be relevant. Politics and national interests may well guide business practice, but neoclassicism regards these as unimportant, or deviations from fundamental and unchanging relationships. The market — a simplified abstraction of conditions that only partially hold in the real world — is the controlling factor, and prices are set by supply and demand in everything: labor, commodities, land, intellectual property, etc. The market is efficient, rational, fair, not affected by historical factors and works best when unhindered by social or political constraints. Both workers and industrialists are better off under market economies, and governments should simply set, interpret and enforce the rules. Indeed all resources are optimally allocated by the market, which is self-correcting: slumps and unemployment occur rarely, and only because the market is being kept from its proper functions. Neoclassicism began in the writings of Adam Smith and has culminated in globalization, which has brought astonishing growth to China, India and other countries previously languishing under socialist economies. {115-8} {120-1}

Neoclassicism is simple in principle, but uses statistics to collect representative data, and often a good deal of advanced mathematical data in its analyses. The basic principles of neoclassical economics are well set out in textbooks and Internet sites {5-9} — such matters as supply and demand, output, growth and capital, inflation and unemployment, money supply, trade, taxation, trades unions, competition, government spending: there is hardly an aspect of modern life in which economics has not something to say. {10-11}

Neoclassical economics is still the lingua franca of the business press, and students must reproduce its teachings to get their grades. Nonetheless, the financial crash has not only opened eyes to dubious banking practices but called into question the foundations of our market economy. {12} Critics allege:

1. Economic forecasting has been ineffective: few economists predicted the current crisis, {13-14} or previous ones. {15}

2. Reliance on economic theory, particularly market efficiency, has played a large part in the financial disasters of the last few years. {16-17}

3. Globalization and the free market have created unemployment in western countries, and widening inequalities in the third world. {18-21}

4. Even the basic tenets of economics are shaky or demonstrably false. Economic models are remote from business realities, many models being 'blackboard diagrams' or 'armchair theorizing', sometimes more obscured than illuminated by mathematical treatment. The world simply isn't as economics supposes.{22-25} {132}

Psychological Foundations

Economic theories generally see human beings are rational creatures propelled by narrow self-interest who nonetheless have sufficient knowledge and ability to make consistently sensible judgments toward their subjectively defined ends. 'Homo economicus' attempts to maximize utility as a consumer, and economic profit as a producer. {26}

Much of economic theory is through modeling of diagrams, which is basically a calculus of nineteenth-century utilitarianism. {27} Human beings are not rational, {28} however, do not have a clear view of opportunities and their consequences, and are not always self-seeking in the manner supposed. {29} No company would survive if its workforce were so constituted, and indeed most try to inculcate a sense of loyalty, common purpose and service to their customers. {30}

As the advertising industry knows, sales in everyday items are not made by appealing to reason but by tapping into emotional needs.

Economic does not sufficiently take cultural attitudes into account, {81} which differ markedly across the world. Unlike Americans, for example, the Japanese expect lifetime employment for lifetime loyalty to a company, and commonly buy government debt. {31}

Why has economics, and neoclassical economics in particular, become so influential? Because, critics argue, it allows companies to sidestep ethical considerations and need for social change by claiming they are simply following market dictates. Some think this is socially unwise, and that maximizing profits to shareholders leads to shortsighted policies, where the need to watch the share price and prevent takeovers inhibits long-term investment. {44}

Only a minority {85} {90} suppose that economics is worthless. Economists are continually compiling the statistics of matters vital to economic life, and trying to understand them. {8} {84} Criticism is leveled at sterile arguments over models that have little currency outside academic journals, and/or which justify wrong-headed business practices. {86-87} Economists do not claim their systems entirely model the real world, of course, only that they give useful predictions. Indeed they often model in the limits of knowledge and talk about rational expectations. Nonetheless, many concepts do derive from simplistic models, and the temptation of all schools, from Marxist to Monetarist, is to argue that their prescriptions have not been followed rigorously enough when results differ from expectations.

Over-Simplistic

Keen {23} provides a detailed critique, which is very briefly summarized here.

Neoclassicists generally adopt a model like this: Economic behavior can be modeled by a single consumer, endowed with rational expectations, who aims to maximize his utility from consumption and leisure. His income derives from the profits of a single firm in the economy, of which he is sole owner and in which he is sole worker. The profits he receives are the marginal product of capital times the amount of capital employed by the firm. The wages he receives are the marginal product of labor times the hours he works in the firm. The output of the firm determines output today, and today's investment (minus depreciation) determines tomorrow's capital stock. The single consumer/owner/worker decides how much of current output to devote to investment, and how many hours to work, so that the discounted expected future value of his consumption plus leisure plan is maximized. Technology facilitates the expansion of production, the expansion growing at constant rates but subject to random shocks The shocks may alter the equilibrium levels chosen for labor and investment, but the system will gravitate to equilibrium conditions. {32}

Supply and Demand

Mainstream models generally assume that a. individual preferences can be quantified, and b. they remain unchanged even though income rises. Models then reduce a complex society to an idealized citizen whose needs can be measured in units of satisfaction or 'utils'. Cook an adequate meal at home or go out to dinner? The choices could be measured and compared in terms of 'utils', and be extended to heating, clothing, freedom of action, and so on. Individuals would rationally aim to maximize their amount of 'utils'. Curves linking the same totals of 'utils' were curves of the same satisfaction, and are therefore called 'indifference curves'.

The indifference curve can be quantified if know the value of x and y utils — i.e. the prices of x and y — and the income of the individual concerned. By a. holding the income fixed, b. reducing the price of one of the utils (say x) and c. keeping the price of the other for the other util (y) constant, a demand curve is constructed for x . It is downward sloping and applies only for the one individual. Substitution is likely if income increases (the individual buys ground coffee in place of instant), but the substitution effect can be neutralized by retaining the shape of the indifference curve while shifting its position (the Hicksian compensated demand curve). In this way {93} — without reference to empirical data — the demand curve receives its characteristic shape.

Unfortunately, once the single individual is replaced by a society of interacting individuals (i.e. a more realistic picture, though still hampered by simplistic 'utils') the demand curve can adopt almost any shape. Indeed, since individuals differ in their preferences and earning abilities, the Law of Demand will only apply if there is just the one consumer, a highly unrealistic scenario that is nonetheless employed to argue against redistributive economic policies. {37}

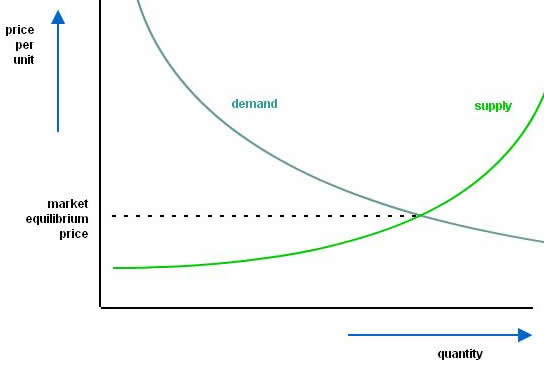

Price is Set by Supply and Demand

The clearing price marks the intersection of

the demand and supply curves for a commodity, and so a point of equilibrium, towards

which prices will naturally gravitate. The principle is intuitively obvious, but only

applies to the individual firm/consumer. In fact: {33}

1. Companies do not price

their products in this way.

2. The demand and supply curves are not derived empirically,

but constructed as models to be substantiated by what data exists, often very limited.

3. The supply and demand curves are not necessarily of their supposed shape,

or only so in special circumstances (different shopkeepers have different costs and

prices).

4. Much pricing is dictated by social expectations, i.e. custom and advertising

rather than supply and demand.

5. The model doesn't so much idealize the situation

as conflate complex situations which would (individually) give more useful results.

Self-Refuting

Equally damaging is the internal inconsistency of economics: the discipline can be logically disproved in its own terms. {34} The supply curve doesn't exist, for example, because the concept of marginal cost of production on which the supply curve is built ( the additional expense incurred in producing just one more item of production) rests on the error of supposing that a small figure equates to zero. Correct that error, and a competitive market will set a price above the marginal cost, which makes it impossible to draw a supply curve independent of the demand curve. {35}

Capital and Labor Markets

Now a little more detail from Keen. {82} Capital in economics means both machinery and sums of money. The two are not equivalent because (as Sraffa modeled {36}) commodities are produced by factors of production. Companies convert labor and capital to goods for supply to households, and households must return something to companies to complete the cycle. Since households are not factories and do not supply goods, that something must be labor and capital. The standard explanation is that profit-maximizing firms will hire (employ) that capital to derive a profit where its marginal contribution to output just equals the cost of hiring that capital. The cost of hiring is the rate of interest charged on the capital, and its marginal contribution is the rate of profit earned on that capital for one additional item of output.

To take the matter in steps:

1. Change in income of a company =

a. change in wage bill +

b. change

in profit

2. Splitting the change in profit into two components: change in income of a company =

a. change in wage bill +

b. rate of profit multiplied by

change in capital +

c. amount of capital multiplied by the change in the rate

of profit.

In the simplest case, both a and c are zero, and any change of income comes from hiring more staff. That leaves b:

Change in income of a company = rate of profit multiplied by change of capital.

Which gives the mainstream economist's relationship (at the marginal cost of production level):

Change in output due to a change in capital = rate of profit.

3. In real life, however, changes in capital will affect wages and the rate of profit. The aggregate relationship is then:

The change in output due to change in capital equals:

d. change

in wages due to a change in capital (not zero) +

e. rate of profit +

f. amount

of capital multiplied by the change in the rate of profit due to the change in capital

( not zero).

The rate of profit will therefore not equal the marginal product of capital unless d and f exactly cancel each other out, which is rarely the case. A similar argument applies to wages. As a consequence, the distribution of income is not meritocratic, nor determined by the market, but reflects the power of various classes and professions. Money traders, bank and managerial staff do not have their high wages because they are more productive and/or contribute more to the marginal product of labor and capital, but because their high wages are part of an accepted socio-economic structure, a circular argument for the status quo. {30} In the high debt situations of today, increasing wages for the many (i.e. contrary to austerity programs) may indeed create the necessary inflation better than printing money.

More damaging to the neoclassical theory of supply and demand is the need for a benevolent dictator to organize matters, a key but clearly nonsensical requirement. {38}

Static versus Dynamic Scenarios

Situations are always changing, and to assume that actual situations are merely transient states on their way to equilibrium conditions shuts the door to more helpful treatments. Keynes' work addressed the persisting unemployment of the 1930s, though his policies did not become orthodoxy until much later. {39} Minsky's modeling of bank share, wage share and unemployment disclosed a 'death spiral' of debt that would not exist in a static world. {40} {41} The well-known Phillips relationship between inflation and unemployment was only one result of adding a time factor to economic modeling. {42}

Modifications

Economists, like academics generally, are a community with many strands of thought. Modifications to mainstream neoclassicism include:

1. Austrian school: similar to neoclassicism but with less emphasis on market equilibrium. {45-46}

2. Post-Keynsian economics: builds on the work of Keynes {47-48} and Kalecki: {49-50} more emphasis on uncertainty.

3. Complexity and econophysics: attempts to apply nonlinear dynamics to stock markets and economic issues: much is proprietary to companies engaged in the work. {53-54}

4. Evolutionary economics: treats the economy as evolving systems, sometimes with complexity. {55-57} {76}

5. Monetarism: associated with Milton Friedman and concentrates on the money supply: influenced waned in the 1980s.{58-59}

More divergent economists have difficulty getting their papers into mainstream journals, but publish widely on the Internet. Their sites provide some of the detail missing from this section.

1. Yves Smith at Naked Capitalism.

2. Michael Hudson at his Michael Hudson blog.

3. Dan Denning at Daily Reckoning.

4.

Max Keiser at The Keiser Report.

5. Mish Shedlock

at Global Trend Analysis.

6. Chris Martenson at Peak Prosperity.

7. Bill Mitchell on the Billy blog.

8. Steve Keen on his blog.

9. Edward Harrison at Credit Writedowns.

10. New Economic Perspectives at the University

of Missouri.

11. Institute for New Economic

Thinking.

12. Levy Institute at Bard

College.

13. Zero Hedge.

14.

Wall Street Examiner.

Alternatives: Multicentric Organizational Models

A less popular group of economic theories derives from the work of David Ricardo (1772-1823), Thorsten Veblen (1857-1929), Karl Polyani (1886-1964), Piero Straffa (1898-1983) and John Kenneth Galbraith (1908-2006).

Ricardo {101-2} concluded that incomes of most workers would not rise above subsistence levels, which was indeed the case for much of the nineteenth century.

Veblen's {103-4}The Theory of the Leisure Class (1898) saw capitalists as modern manifestations of the ancient warrior class, gaining wealth and power through predatory manipulations. Far from being free and rational creatures, consumers were culturally induced to show off their wealth by 'conspicuous consumption'.

Polyani's The Great Transformation (1944) {105-6} argued that the market is always embedded in a cultural and political context, and the transformation of workers, nature and monetary gold into 'fictional commodities was responsible for the destruction of community, environment and democracy. {122}

Straffa {51-52} reestablished political economy through commodities produced by commodities, and was critical of simplistic and atomistic approaches. Based on Ricardo's writings, he constructed equations that would yield consistent prices, something he demonstrated that neoclassical economics was unable to do.

Galbraith {107-8} was a popular author who argued that mathematical modeling was unrealistic, often resulting in 'certainties' that misled their authors, (as did derivatives in the financial crash). He stressed the power that corporations tend to seek, often through advertising, and the increasing numbers of specialists they employ: scientists, engineers, lawyers, accountants, marketing specialists, government liaison officers, etc., the so-called 'technostructure'. His New Industrial State (1967) identified eight controlling strategies:

1. Creation of consumer demand by advertising.

2. An aim for steady profit that provides dividends for stockholders and reduces outside loans.

3. Collective bargaining with 'tame' trade unions.

4. Prices set by companies and industries rather than by markets.

5. Relentless expansion in each market sector by competition or takeovers.

6. Funding and therefore control of relevant university research.

7. Influence on government policies and budgets.

8. Identification with popular culture, spending revenues gained in avoiding tax on public relations exercises.

Gloomier outlooks generally prevail in these models. {119} Workers are not necessarily better off under market economies because companies aim for wealth and power rather than the most efficient satisfaction of consumer wants. Unless prevented by legislation, competition is a race to the bottom, and wages must trend towards subsistence. Industrialists are equally vulnerable unless they have exclusive access to scarce resources, and often depend on governments and lobbying to maintain or extend their operations. Reducing everything to commodities priced in money terms by the market devalues human beings and encourages over-exploitation of natural resources. {111} Alongside private affluence grows public squalor because profit is internalized by market forces but social costs are externalized. Companies are happy to use a workforce housed, fed and educated by the country concerned, but see no responsibility to that country beyond paying the going wage. American companies in particular avoid their social responsibilities by off-shoring and widespread tax avoidance. {112}

In practice, as the country forecasts show, economics cannot be divorced from politics and national interests. Globalization has unfairly benefited the richer classes in both the west and developing countries, with the main burden of social costs falling on a dwindling middle class at home and on the poor in developing countries. According to US government figures, for example, the inflation-adjusted incomes for the lowest 20% of households have increased only 2% over the 1979-2004 period, but incomes of the top 20% have increased 63%. The top one percent have done even better, with a 154% increase over this period. Even in 2000, a UN University study found that the bottom 50% of the world owned only 1% of its wealth, while the richest 1% owned 40% of global assets (land, buildings and financial assets). {110} Banks have been subsequently bailed out with public funds, and the military-industrial complex has pushed for armed intervention overseas, receiving government contracts that are often poorly supervised. {113-4}

Alternatives: Marxist Models

Marxism of course derives from Karl Marx (1818-1883) but was developed further by Vladimir Ilyich Lenin (1870-1924), Gramsci (1891-37) and Spike Peterson, and many others.

Marx laid the foundations of this most important group of economic theories through a penetrating critique of nineteenth century capitalism. His three-volume study, simply called Capital, looked at the nature of capitalism: where it came from, how it worked, what was wrong with it, why it was a temporary phase in human history, and what was needed to speed up its demise. He studied the ugly factory towns and their exploitation of labor under the most oppressive conditions, and took from David Ricardo and Thomas Malthus the view that what allowed the exchange of commodities was the amount of labor time involved. Marx was more philosopher than economist, but his 'dialectic materialism' (as his system came later to be called) envisaged: {123}

1. All phenomena are interrelated and interdependent: Marxism is not reductionist.

2. All societies are in a state of change, and even markets do not tend towards equilibrium.

3. Change is evolutionary: primitive communism evolved into ancient civilizations, and these into feudal Europe and then capitalism, which in turn will evolve into communist societies.

4. Change is driven by contradictions or tensions between classes.

5. The basic reality for men is not ideas but material existence: food, housing, fighting ill-health, struggling with others, etc.

6. From these material phenomena come men's ideas of himself and his purpose in the world.

7. Relationships between these material phenomena are regular, and may be studied in a scientific way, though the approach must be holistic and the underlying forces need some ferreting out: people's lives are often driven in certain directions while they themselves are preoccupied with trivial matters.

8. The scientific approach must combine theory and practice: detached observation lacks the essential contact with reality.

9. Capitalists make their profits from 'surplus value', the difference between the sale price of an item and the average socially necessary amount of labor time spent in bringing it to market: that labor time included creation of food and housing, construction of plant and marketing, etc.

10. Workers own only their labor, and are locked in a continual struggle with capitalists for a share of the latter's profits.

11. Though the extraction of surplus value from labor would drive wages down to subsistence levels, the inevitable shift to using less labor and more capital would lead to business cycles and eventually the destruction of the capitalist system.

Lenin argued that capitalists' investments were more easily protected under imperialism, which paid little heed to local needs or cultures. More famously, he led the Bolshevik Revolution in Russia, though the Stalinist Soviet empire was a parody of Marx's views of an ideal society. {124}

Gramsci modified Marxist thought to take more account of civil society and cultural controls. {125}

Peterson surveyed how capitalists cut labor costs by using women in part-time, non-unionized and poorly-paid work. {126}

Contemporary Marxists have a long catalogue of social ills, even for a rich country like the USA. Only a minority of workers belong to a trade union, or have health insurance. Ideology is propagated throughout society by advertising, education and the media. Capitalists employ divisive social issues in political campaigns to divert interest from more fundamental issues: abortion, immigration and same-sex marriage. The rich get richer at the expense of other classes in America and elsewhere. {127-130}

As in any other branch of economics, Marxism is not without its theoretical problems. If expended labor is the common denominator of price, how are land, labor and capital to be equated? Clearly they are different: capital is mobile, labor much less so and land not at all. Other economic models treat them as necessary inputs to surplus value, and hence profits, but Marxism continues to wrestle with its labor theory of value. {43}

Alternatives: Economics is Fiction

A minority of critics go further and argue that conventional economics acts as a cover, a fig leaf of respectability to power politics. {72} {79-80} Recessions do not simply happen through the interaction of market greed and fear, for example, but are created by banks working with government and big business. {95} {131} Engdahl {77} observes that banks and big business have furthered US globalist ambitions, and will be supported for that reason, even at the cost {78} of American jobs and civil liberties. A summary of Engdahl's analysis (greatly simplified):

Episode |

Players | Action |

Result | Broader Aims/Results |

1893 Panic |

J.P. MorganJohn D. Rockefeller |

Silver outlawedas legal tender. |

1983-7Recession. |

Morgan's acquisitionof steel & railway stock.Rockefeller's consolidationof Standard Oil. |

1907 Panic | J.P. MorganJohn D. Rockefeller | KnickerbockerTrust devalued. | Majorbankruptcies. |

JPM's acquisition ofTennessee Coal and Iron.Federal Reserve System 1913 |

America's entryinto W.W.I 1915-18 | J.P. Morgan |

Rescue of $ 22bn US loansto Britain. | Profiteering by USsteel, chemical andarms manufacturers. |

Europeanpowers weakened. |

N.Y.-led goldexchangestandard 1924-31 |

Edwin Kemmerer /J.P. Morgan |

Capture of SouthAfrica goldsupplies. |

Expansion of UScredit. Corporationstaken over bybig banks. | Roaring Twenties,followed by Great Depression. |

1929-33 Agriculturaldepression |

Fed | Raisesinterest rates. | Increasingcycle of farm andbank failures. |

Fed becomes financierof government debt.US comes offgold standard.Glass-Steagal Act.Rockefeller triumphsover JP Morgan |

War and PeaceStudies 1939-42 | Rockefeller |

Plan to replaceBritish Empire byUS hegemony. |

US companies fundNazi economy. |

Foment European war.Provoke Japanese aggression. |

Peace 1945 |

Banks &US Government |

Exact repaymentof US debtfrom Britain |

Europe dependenton US and US dollar |

Britain dependenton US |

Exclusive Saudi oilrights |

Roosevelt

|

US agreementwithSaudi Arabia. |

British interestsdiminished. |

Saudi oil inexchange for US protection |

Bretton Woodsaccord 1945 |

US governmentUS banks | Internationalcurrenciesfixed against US$. |

Dollar becomeinternationalcurrency. |

Pax AmericanaDollar replaces gold. |

Marshall plan | US government& US banks |

Generous loansforEuropeanreconstruction. | Rapid recoveryof Europeaneconomies. | Markets for US goodsprotected by NATO.

|

Korean War 1950 | US government& US banks | Unificationby N. & S. Korea.Escalatingborder clashes. |

$ 1.2 tn USinvestment inS Korea rescued.Costly war. |

As in Europe:Economic ties withKorea. Increasedmilitary expenditures. |

Currencywar 1967-9 |

US government& US banks |

Prevent Franceleaving gold pool& threatening $. |

France devaluesfranc.Student riots. |

de Gaulle resigns. |

Vietnam War | US governmentRockefeller |

Prevents S.Vietnamgoingcommunist. |

War and sooil, rubber& mineral reserveslost |

Increased militaryexpenditures. |

End ofBretton Woods 1971 |

US government& US banks |

Accord droppedfor floatingexchangerates. $revalued. |

OverseasUS bank branchescreated. |

Expansion of $ holdingsand US debt. |

Oil shock 1973 | US governmentRockefeller |

Iran instructedto raise oil price. |

N. Sea & otheroilfieldsprofitable.Worldwiderecession. |

Petrodollars in US banksloaned to 3rd world. |

Volker shocktherapy 1979 |

US government& US banks |

Impose highinterest ratesto curbinflation. |

Bankruptcies.Wealth re-distributed upwards.IMF more powerful. | Worldwide debtcrises. |

Marketderegulation |

US government& US banks |

Repeal ofGlass-Steagal. |

Growth ofsubprime marketandderivatives. |

Birth ofneoliberalism. |

Stockmarketcrash 1987 | US banks& stock markets | DCT bails outtroubled banks.Japan requiredto devalue |

Continental Illinois,and S & L banksbailed out:$900 bn cost. | US debt beginssteep rise. |

Stockmarketcrash 2000 | US banks& stock markets | Dotcomcompaniesdevalued. | Interest ratescut. |

End of Asianfueling of markets. |

Financial crash2007 | US banks& stock markets | Subprime marketcollapses. | Major bankruptciesand mergers. | Worldwide recession.Austerity measures in middleAmerica and abroad. |

Bank bailouts2008 | US government& US banks | Rescue of USbanks and largebusinesses |

Status quo restored.Moral hazard.Wealthy benefit |

High US and world debt.Approaching endof US century.Investment awayfrom US companiesand models. |

Current Conundrums

Do these views matter? Not on the mainstream business scene, but possibly to companies that need to probe economic realities and see further. What appears in newspapers, and even business magazines, is based on notions that may be out of date, one-sided or simply untrue. Some further considerations:

Monetarism

Monetarism would control growth through the money supply, by the well known equation:

MV = Py

where M is the money supply, V is velocity (turnover), P is the price change and y is real growth. There are several measures of money, and not all are easy to regulate, but the V is the more troubling measure. It's based on psychology, general feelings. For the USA, population growth is about 1.5% p.a., and productivity increases around 2 to 2.5%. From those figures, the country ought to comfortably manage a GDP increase of 3.5-4% year on year. But the velocity of money peaked at 2.12 in 1997, and has been on downward course since, falling to 1.67 in 2009 and leveling off at 1.71 in 2010. The Fed has therefore been printing money to offset this fall in money velocity.

The Fed indeed controls the monetary base, about 20% of the money supply. Banks create the remaining 80%. Between January 2008 and January 2011, the monetary base has been increased by 242%. As that was having little effect, the Fed used other methods to boost confidence. For a while it supported house prices. When that proved impracticable, it turned to another indicator that is closely watched: the stock market, which is now being manipulated. Bernanke is quite open about depreciating the dollar, hoping a fear of inflation — echoed in magazine leaders across the country — will push Americans to consume more. {60}

Keynsian Economics

Keynsian economists, {61} modeling at the end of the Bush presidency, expected a multiplier of 1.54. The 2009 Obama stimulus of $787 bn was to yield an additional $425 bn. Indeed the fiscal deficits amounted to $1.4 tn in 2009, $1.2 tn in 2010, and were projected at $1.6 tn in 2011 and $1.1 tn in 2012, an astonishing $5.4 tn over four years. Unfortunately, when figure came in, the multiplier appeared to be less than 1. Indeed a fuller study by Taylor and Cogan {62} showed that all multipliers were less than one. The Obama stimulus program achieved a multiplier effect of 0.96 at the start of the program, but this fell to 0.67 by the end of 2009, and to 0.48 by the end of 2011. Their work therefore showed that, for each stimulus dollar spent, private sector output would fall by nearly 60 cents. Other studies supported these conclusions. {60}

What went wrong? Nothing said one group of economists: the stimulus package had been a success. {63} Others argued that the stimulus had been wrongly applied, much of it through tax rebates. {64-65} Others again contended that Keynes' theory works only for short periods, for a liquidity rather than a solvency crisis, and for a mild recession with relatively low debt levels at its outset, i.e. with economies with a balanced budget. {60} None of these was true of the financial crash, and Keynsian stimulus packages were no more successful in America than they had been in Japan. The political backlash ended the Keynsian solution to American recession.

Efficient Markets

Are markets efficient? Yes, said Paul Samuelson and host of brilliant economists from Yale, MIT and the University of Chicago in the 1950s and 1960s. {117} A decade later appeared the work of Scholes, Merton and Black on the pricing of options, which won their authors a Nobel prize, and opened the door to the explosive growth of financial futures and derivatives. Intrinsic to these is the normal distribution of risk, that familiar bell curve that pushed severe events so far to the extremes of the curve that major disasters could happen hardly at all. On this was built the value as risk (VaR) concept and the Long-Term Capital Management (LTCM) hedge fund with assets totaling $126 billion. {60}

But stock markets events are not independent of each other but retain some 'memory' of the past, and the better model is one of complexity, where disasters are far more frequent, indeed to be expected. VaR was used to manage risk in the decade that led up to the financial crash of 2008, and contributed to its $60 tn loss. LTCM had to bailed out. {66}

Austrian School: Moral Hazard

Should the big institutions have been bailed out? Not according to the Austrian school of economics that sees bankruptcy as normal, indeed necessary for the financial health of markets. Inefficient companies go into liquidation, losses are written off, and staff are reemployed elsewhere. Indeed propping up ailing companies not only prevent assets being properly employed but adds more debt to balance sheets and creates the danger of moral hazard. Management will not act prudently if mistakes are automatically underwritten by tax payers. {67} {97}

The big banks were bailed out for several reason, however, some valid and some less so.

1. The most compelling was the uncertain result of not doing so. Given the opaque nature of derivatives, no one really knew how far the contagion had spread, and indeed bailouts (it was subsequently disclosed) has been used to support many pillars of American business, not only the named banks and insurance companies. {68}

2. The second is the mutual interdependence of government and finance, which has been the case for centuries. {69} Today, through campaign donations and lobby groups, the larger companies and financial institutions openly bankroll the American political system, and indeed the Obama administration employed representatives of companies that caused the trouble in the first place. {70} Beyond that fact of life lies the sheer power of money. As politics is the pursuit of power, it is inevitable that banking and politics will be closely intertwined. Everything comes crashing down if state finances collapse and public workers cannot be paid. Continuity is essential to business, and companies expect governments to maintain stable trading relationships.

3. Decisive action was imperative, and there wasn't the time to have auditors go through the books and wind down bankrupt companies in an orderly manner. Indeed, many of the assets were difficult or impossible to value properly, and simply marking them to market could have set off chain reactions and brought yet more companies into receivership. {71}

That said, three points are usually made.

1. Wall Street got preferential treatment. Banks in Mexico and southeast Asia were not so lucky. {72}

2. The government could have acted as lender of last resort and simply offered loans as required, reducing moral hazard by insisting principal directors resign when recklessness or incompetence was exposed. {73} {74}

3. Pumping money into their reserves does not necessarily make banks want to lend. The multiplier effect is not a compelling mechanism, and indeed banks lend first and consult their reserve ratios later. {75} Since this is common knowledge in the banking fraternity, some cronyism operated.

Corruption

Contrarian economists go further and contend that mainstream economics has betrayed its principles. Far from being a science, i.e. objective and disinterested, the economics taught at college and published in academic journals is now subservient to those who ultimately (however indirectly) pay the salaries: i.e. banking and big business (see the model below). Michael Hudson, {88} for example, observes that the wealthiest 1% have rewritten the tax laws to a point where they now receive an estimated 66% of all returns to wealth (interest, dividends, rents and capital gains), and a reported 93% of all income gains since the Wall Street bailout of September 2008. To achieve that success, the rich have secured control of the major news media that shape peoples' views, and have used the financial crisis they themselves created to argue for further privatization. The public debt is now too large for everyone to be paid, and the financial interests representing the wealthiest 1% have incorrectly {96} argued that a reduction in social services, education, Medicare and upkeep of local amenities is imperative. Books have to be balanced, they argue, forgetting that productivity increases will cover expense, and that sovereign states are not businesses but can print money, as they famously did in bailing out Wall Street. The problem in fact, contends Hudson. {89} is not social security and the like, which can be paid out of normal tax revenue, as in Germany's pay-as-you-go system, but the lopsided treatment of real estate, oil and gas, natural resources, monopolies and the banks, which unfairly benefit from light taxation and tax loopholes.

Some writers indeed argue that economics has never been a science but an elaborate justification of the status quo. Routh: 'By leaving this [power] out, and thus separating itself from politics, economics has become an arrangement for preventing the citizen and student from seeing how he is governed.' {91} And: 'Of course this neglect of the real world in favour of creations of the mind is a leading feature of orthodox economics. That it is generally accepted gives it academic respectability and removes the danger that economics might be used as an instrument in reshaping the world.' {92}

The financial crisis is not an aberration, critics of gloablism argue, {98} but part of a carefully orchestrated policy to run a society on debt — a debt forgiven banks by bailouts but maintained in student loans, mortgages, and business loans. Free money (quantitative easing) furthers the interests of the banking and military machines but not the ordinary citizen. On the latter's default — and defaults are inevitable — the funding institutions pocket the collateral, further increasing their wealth and political influence.

Citizens of the USA and EEC are therefore coming under the same IMF and World Bank policies that advanced the interests of the rich countries over those of the third world. {99} Money is an essential element of capitalist societies, but financial systems that create money out of money are parasitic, not supportable in the long run, and debilitating because they drain resources from areas where investment is most needed: entrepreneurs, local businesses and manufacturing industries. {94} Debt redemption and/or civil disorder can be historic consequences, but a gradual deterioration in business and social well-being seems far more likely in America, where there is yet hardly a trace of the labor rallies and antiwar protests that galvanized politics in the last century.

Validity

Much of this page represents minority views, particularly in Engdahl's case. {83} Wouldn't they enjoy greater currency if there was any truth to them? And the supposed problems of neoclassical economics, how could they have escaped detection for so long?

One answer may be that we often don't want to know of shortcomings that might damage pride in our institutions. A traditional American model, for example, would include:

Media: that promote an image of balance and fairness, supporting

American values and reporting on world events from a national viewpoint.

Government:

that legislates for Americans fairly at home and furthers American interests abroad.

Colleges: that educate Americans in civic values and employable skills.

Corporations:

that employ Americans at home and nationals in their overseas subsidiaries.

Once the influence of money is factored in, however, a more unsettling picture emerges:

Similar models could be built for other economic systems — the middle east, China, the third world — and doubtless the results would be even more disturbing. All societies share common beliefs, indeed require them to function at all, and if many are fictions, it could be argued they are nonetheless 'necessary fictions'. Yet they cause immense problems at the boundaries of power blocks where mindsets collide, and charges of 'commies' or 'mad mullahs' are met with demonstrations against 'American imperialism' or 'the great Satan'.

What can be done? At least appreciate the alternatives to mainstream economics, this page argues, and take a cool look at political realities. eBusinesses with foreign partners and/or customers will not succeed unless cultural differences are understood, respected and harnessed to the enterprise.

Points to Note

1. Neoclassical

economics and the range of criticisms it faces today.

2. Alternative economic

models and their Internet sites.

3. The financial crash and range of proposed

solutions.

Questions

Questions

1. What are the problems with neoclassical economics?

2. Make a case for

neoclassical economics.

3. What do critics blame neoclassical economics for?

4. Construct an institutional model for China.

Sources

and Further Reading

Sources

and Further Reading

1. EU-U.S. Free Trade Deal Offers Painless Stimulus

for Both. Bloomberg.

June 2012.

2. The End of Free Trade? High tariffs and currency wars cost us big

in the 1930s. We can avoid making the same mistakes again by Douglas

A. Irwin. W.S.J.

October 2010.

3. Neoliberalism. Everything falls apart. Economist.

July 2011.

4. Free trade: Way ahead 'is openness, not protectionism' by John Paul

Rathbone.

F.T. June 2012.

5. 9 Best Economics Websites. Topsite.

Accessed July 2012.

6. Top 25 Best Economics Websites. Top

Sites Blog. 2011.

7. The 7 best sites for learning economics for free. FreeConHelp.

Accessed July 2012.

8. The World in the Model: How Economists Work and Think by

Mary S. Morgan. C.U.P. 2012.

9. Economics by Walter J. Wessels. Barron's Educational Series, 2006.

Clear summary: one of many excellent books on the market.

10. The Undercover Economist by Tim Harford. Abacus, 2007.

Extensive reviews on Amazon.

11. Freakonomics: A Rogue Economist Explores the Hidden Side of Everything

by Steven D. Levitt Penguin, 2007. Extensive reviews on Amazon.

12. Neoliberalism: A Critical Reader by Alfredo Saad-Filho and

Deborah Johnston (eds.) Pluto Press. 2005.

13. Economic Forecasting and Policy by Nicolas Carnot. Palgrave

Macmillan, 2011. p 23.

14. The Failure to Forecast the Great Recession by Simon Potter.

Federal

Reserve Bank of New York. November 2011.

15. The Economic Forecasts are Wrong, Which is Probably Good News

by Len Burman. Forbes.

February 2012.

16. Crisis Economics: A Crash Course in the Future of Finance by

Nouriel Roubini. Penguin, 2010.

17. Panic: The Betrayal of Capitalism by Wall Street and Washington

by Andrew Redleaf and Richard Vigilante. Richard Vigilante Books, 2010.

18. The Strange Non-death of Neo-liberalism by Colin Crouch. Polity,

2011.

19. Neoliberalism: Myths and Reality by Martin Hart-Landsberg.

Monthly

Review. April 2006.

20. Neo-classical economics: A trail of economic destruction since

the 1970s by Erik S. Reinert. Real

World Economic Review. 2012.

21. The Political Economy of Development: The World Bank, Neoliberalism

and Development Research (Political Economy and Development) by Kate

Bayliss, Ben Fine and, Elisa Van Waeyenberge (eds.) Pluto Press. 2011.

22. Neo-classical Economics as a Strategem against Henry George

by Mason Gaffney. NTLWorld.

July 2004.

23. Debunking Economic: The Naked Emperor Dethroned by Steve Keen.

Zed Books, 2011. Combative and untidy book, but worth persevering with.

(A better start is made with Routh's book: see 90 below.)

24. The Economics Anti-Textbook: A Critical Thinker's Guide to Microeconomics

by Rod Hill and Anthony Myatt. Zed Books, 2010. Simpler approach than

Keen's book.

25. Economics for the Rest of Us: Debunking the Science That Makes

Life Dismal by Moshe Adler. New Press, 2011. Popular but critical

treatment of two central tenets of mainstream economics.

26. The Prospects for Homo economicus. A new fMRI study debunks the

myth that we are rational-utility money maximizers by Michael Shermer.

Scientific

American. June 2007.

27. The History of Utilitarianism. Stanford

Encyclopedia of Philosophy. March 2009.

28. The End of Rational Economics by Dan Ariely. Harvard

Business Review. July 2009.

29. A Nobel That Bridges Economics and Psychology by Daniel Altman.

N.Y.T.

October 2002.

30. 23 Things They Didn't Tell You about Capitalism by Ha-Joon

Chang. Penguin, 2010. 'Thing' 5.

31. In Japan, a Tenuous Vow to Cut by Hiroko Tabuchi. N.Y.T.

September 2011.

32. Keen, 2011. pp 263-4.

33. Keen, 2011. Chapter 3. Argued in more detail than this brief

summary suggest: Keen considers the work of Gorman, of Sonnenschein, Mantel

and Debreu, of Mas-Coell, of Mankiw, of Sippel and others.

34. Debunking Economics. DebunkingEconomics.

Steve Keen's website.

35. Keen, 2011. Chapter 4.

36. The Production of Commodities by Means of Commodities: Prelude

to a Critique of Economic Theory by Piero Sraffa. O.U.P., 1960.

37. Ha-Joon Chang, 2010. 'Things' 3 and 14.

38. Keen, 2011. p. 59.

39. Keynesian Economics by Alan S. Blinder. Library

of Economics and Liberty. Accessed July 2012.

40. The Minsky Moment by John Cassidy. New Yorker. February

2008.

41. "Minsky Phases" tactical asset allocation model.

MacroAnalysis.

Accessed July 2012. Application only, no theory.

42. Phillips Curve by Kevin D. Hoover. Library

of Economics and Liberty. Accessed July 2012.

43. Marxism by David L. Prychitko Library

of Economics and Liberty. Accessed July 2012.

44. How Shareholders are Hurting America by Jesse Eisinger ProPublica.

June 2012. With a good discussion.

45. Austrian School of economics. Conservapedia.

July 2012.

46. What is Austrian Economics? Ludwig

von Mises Institute. Accessed July 2012.

47. Keynesian Economics in a Nutshell. Maynard

Keynes. Accessed July 2012.

48. John Maynard Keynes (1883-1946 ) Library

of Economics and Liberty. Accessed July 2012.

49. Political Aspects of Full Employment by Michael Kelecki. MR

Zine. June 2010.

50. The Kalecki hypothesis. Rabble.

July 2010.

51. Sraffian economics vs. Post Keynesian methodology by Matias

Vernengo. Naked

Keynesianism. March 2012.

52. Value and distribution in the classical economists and Marx by

P. Garegnani. Oxford

Economic Papers 1984.

53. Econophysics and the Complexity of Markets by D. Rickles PhilSci-Archive.

2008. Readable introduction, but needs some familiarity with economics

terms.

54. Introduction to Econophysics: Correlations and Complexity in Finance

by Rosario N. Mantegna. C.U.P., July 2007. Requires a good math/physics

grounding.

55. Darwinian Economics. Darwinian

Economics. Friendly introduction.

56. The Social and Economic Background of the Modern Developed Nation-State

by Keith Hudson. Evolutionary

Economics. Accessed July 2012.

57. Evolutionary Economics. Cosma Rohilla Shalizi at the University

of Wisconsin. February 2011. Reading list.

58. Monetarism by Bennett T. McCallum. Library

of Economics and Liberty. Accessed July 2012.

59. Chapter Seventeen: Lecture Notes — Monetarism. Lecture Notes

on Macroeconomics. EconWeb

1996-2004.

60. Currency Wars: The Making of the Next Global Crisis by James

Rickards. Penguin 2011. Chapter 9.

61. The Job Impact of the American Recovery and Reinvestment Plan

by Christina Romer and Jared Bernstein. Report prepared by the Council

of Economic Advisers, January 9, 2009. Council

of Economic Advisers.

62. The Obama Stimulus Impact? Zero by John B. Taylor and John

F. Cogan. W.S.J.

December 2010.

63. CBO reports stimulus package was a major economic success by

Jay Bookman. Jay

Bookman Blog. November 2011.

64. Pros and Cons of Obama's Stimulus Package by Deborah White.

About.com

Guide. Accessed September 2012.

65. Book Review: Against Thrift by James Livingston. Michael Rosenwald.

Bloomberg.

November 2011.

66. What Was the Long-Term Capital Management Hedge Fund and the LTCM

Crisis? by Kimberly Amadeo. About.Com

Guide. January 2012.

67. Moral Hazard and the Financial Crisis by Kevin Dowd. Cato

Journal. 2009.

68. Secret Fed Loans Gave Banks $13 Billion Undisclosed to Congress

by Bob Ivry, Bradley Keoun and Phil Kuntz. Bloomberg.

November 2011.

69. J. Bradford DeLong's Awesome Presentation On The History Of The

Bank Bailout by Gus Lubin. Business

Insider. April 2010.

70. Book Review: 'Bailout' by Neil Barofsky, or: Why I'll Never Work

in Washington D.C. by Jordan Terry. Stone

Street Advisors. August 2012.

71. Economic Meltdowns: Let Them Burn Or Stamp Them Out? Investopdia.

July 2008.

72. The Web of Debt by Ellen Hodgson Brown. Third Millenium Press. 2008.

Chapters 22 and 26.

73. Will the Central Bank Bailouts Ever End? by Randall Wray. Multiplier

Effect. February 2012.

74. What We Can Learn From Chile's Financial Crisis by Mary Anastasia

O'Grady. W.S.J.

September 2008.

75. Keen, 2011. Chapter 14.

76. What have the economists ever done for us? by Andrew G Haldane.

Vox.

October 2012

77. Gods of Money: Wall Street and the Death of the American Century

by F. William Engdahl. EditionEngdahl 2010.

78. Super Imperialism — New Edition: The Origin and Fundamentals

of U.S. World Dominance by Michael Hudson. Pluto Press 2003.

79. Future Money: Breakdown or Breakthrough by James Robertson. Green

Books 2012.

80. Consumer Price Index by John Williams. Shadow

Statistics. May 2012. Figures regarded as controversial by mainstream

sources.

81. The Skeptical Economist: Revealing the Ethics Inside Economics

by Jonathan Aldred. Routledge 2010.

82. Keen, 2011. Chapter 7.

83. The Making of Global Capitalism by Sam Gindin and Leo Panitch.

Verso 2012. Also argues close association of capitalism with US policy.

84. Global Wealth Report 2011. Credit

Suisse. October 2011.

85. What is wrong with economics? by 'afaq'. Anarchist

Writers. November 2008. A far-ranging critique.

86. Economists and the Powerful by Norbert Häring and Niall

Douglas. Anthem Press 2012. Role of power in the economy.

87. Reality Economics by Michael Hudson. Counterpunch.

December 2012. Summary of Häring and Niall Douglas.

88. The Bubble and Beyond: Fictitious Capital, Debt Deflation and Global

Crisis by Michael Hudson. Islet. 2012.

89. America's Deceptive Fiscal Cliff: The Ideological Crisis Underlying

Today's Tax and Financial Policy by Michael Hudson. Counterpunch.

January 2013.

90. The Origin of Economic Ideas by Guy Routh. Macmillan. 1977.

A well written, indeed entertaining, critique of economics that anticipates

many of Keen's objections.

91. Routh 1977, p. 24.

92. Routh 1977, p. 288. A comment on Keynes, but applying throughout the

history of economics.

93. Keen, 2011. Chapter 2. Also see Derive Demand Curve From Indifference

Curve. Economist.Wikidot

. December 2011, Deriving the demand curve. WikiEducator.

February 2012, etc.

94. Manufacturing is a small but increasing component of the US economic

scene. See: The Myth of U.S. Manufacturing Decline by John V. Walsh.

Counterpunch.

October 2012.

95. The Shock Doctrine by Naomi

Kline. Metropolitan Books 2007. Summary at NaomiKline.Org.

96. The Battle for Social Security: From FDR's Vision To Bush's Gamble

by Nancy J. Altman. Wiley 2005.

97. Lack of Trust – Caused by Institutional Corruption – Is Killing

the Economy. Washington

Blog. May 2012.

98. Bail-in and the Confiscation of Bank Deposits: The Birth of the

New Financial Order by James Corbett and Michel Chossudovsky . Global

Research. April 2013.

99. Economic Espionage as an Instrument of “Financial Warfare”

by Lars Schall. Global

Research. July 2013.

100. International Political Economy: Contrasting

World Views by Raymond C. Miller. Routledge, 2008.

101. The Worldly Philosophers: The Lives, Times and Ideas of the Great

Economic Thinkers by Robert Heilbroner. Simon and Schuster, 1986.

102. David Ricardo. Library

of Economics and Liberty. Accessed August 2013.

103. Thorsten Veblen on the predatory nature of capitalism by Janet

Knoedler in Introduction to Political Economy by Charles Sackrey and Geoffrey

Schneider. Dollars and Sense, 2002.

104. Higher Learning in America: A Memorandum on the Conduct of Universities

by Businessmen by Thorsten Veblen. Huebsch, 1918.

105. The Great Transformation: The Political and Economic Origins of

Our Time by Karl Polyani. Rinehart, 1944.

106. The Revenge of Ideas by Fred Halliday. Open

Democracy. September 2008.

107. John Kenneth Galbraith: His Life, His Politics, His Economics

by Richard Parker. Farra, Strauss and Giroux, 2005.

108. John Kenneth Galbraith. John Kenneth Galbraith, economist

and public intellectual, died on April 29th, aged 97. Economist.

May 2006.

109. When Corporations Rule the World by David C. Korten. Berrett-Koehler,

2001.

110. The World Distribution of Household Wealth by James Davies,

Susanna Sanderström and Edward Wolff. United Nations University:

Helsinki, 2006.

111. Alternatives to Economic Orthodoxy by Randy P. Albeda, Christopher

E. Gunn and William Wallers (eds.). Sharpe, 1987.

112. The price isn’t right. Economist.

September 2012.

113. Defence and Security. Transparency

International. Accessed August 2013.

114. The Military-Industrial Complex It's Much Later Than You Think

by Chalmers Johnson. Global

Research. July 2008.

115. Models in Political Economy by Michael Barrat Brown. Penguin,

1995.

116. Capitalism and Freedom by Milton Friedman. Univ. Chicago Press,

1962.

117. Economics by Paul A. Samuelson. McGraw-Hill,

1970.

118. Economics Explained: Everything You Need to Know about How the

Economy Works and Where It's Going by Robert Heilbroner and William

Milberg. CUP, 1995.

119. Mad Money: When Markets Outgrow Governments by Susan Strange.

Univ. Michigan Press, 1998.

120. The Birth of Plenty: How the Prosperity of the Modern World was

Created by William J. Bernstein. McGraw-Hill, 2004.

121. The Wealth and Poverty of Nations: Why Some Are So Rich and Some

Are So Poor by David S. Landes. Norton, 1998.

122. The Health of the Planet and the Wealth of Nations by Andrew

Simms. Pluto Press, 2005.

123. The Communist Manifesto by Karl Marx and Friedrich Engels.

Appleton-Century Crofts, 1848/1955.

124. Imperialism: The Highest Stage of Capitalism by V.I. Lenin.

International Publishers, 1917/1939.

125. Selections from the Prison Notebooks by Antonio Gramsci. International

Publishers, 1926-36/1971.

126. A Critical Rewriting of Global Political Economy: Integrating

Reproductive, Productive and Virtual Economics by V. Spike Peterson.

Routledge, 2003.

127. Marxism, For and Against by Robert Heilbroner. Norton, 1980.

128. Reclaiming Marx's Capital; A Refutation of the Myth of Inconsistency

by Andrew Kliman. Lexington Books, 2007.

129. The Structure of Marx's World-View by John McMurtry. Princeton

Univ. Press 1978.

130. International

Viewpoint. Many articles and archive on international socialism.

Accessed August 2013.

131. Wall Street’s Secret “Economic Endgame”: Making the World Safe

for Banksters, Syria in the Cross-hairs by Ellen Brown. Global

Research. September 2013.

132. The Irreconcilable Inconsistencies of Neoclassical Macroeconomics:

A False Paradigm by John Weeks. Routledge, 2012.